When I read the headline, I thought the article would be about the difficulty of finding a return in the current low yield environment. It turns out its on something completely different (excerpt):

In search of higher yields

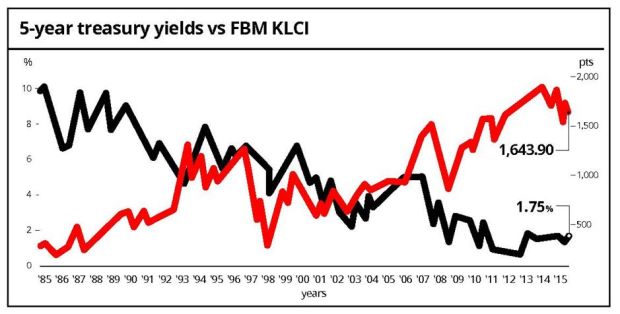

THE correlation between yields and stock markets are clear to see. When yields are high, stock markets are down. When yields are down, money pours into the stock market, and hence it goes up (see chart).

From the chart, it is obvious that since the Fed launched quantitative easing in 2009, rates have sunk to all time lows – close to zero. Meanwhile stock markets start rising when money is in search of yield and growth. Thus when yields are low, the stock market moves up.

An interesting observation from the chart is the huge gap between rates and the stock market from 1985 to 1993.

In 1985, the US Treasury 5-year notes were offering yields of above 10%. Not surprisingly, investors would gladly take their money out of the markets and put it in treasury notes or bonds, which are almost risk free.

Now, as the yields started to drop, notice how the stock market starts inching up. This is because investors start to realise that bonds can no longer give them the best yields, and thus they shift their money into the stock market.

From 1993 to 2006, yields on the 5-year note and the stock market moved almost in tandem.

Over that period, the yields moved in a band of between 4% to 6%. At this level, bond yields and stock market returns are about equal. So investors are interchanging; when yields go closer to 4%, they shift their assets into the stock market. Then when yields move up again, they shift back out of equity markets and into treasury notes….